Joint Economic Report Spring 2013: German Economy Recovers – Long-Term Oriented Economic Policy Required

Research

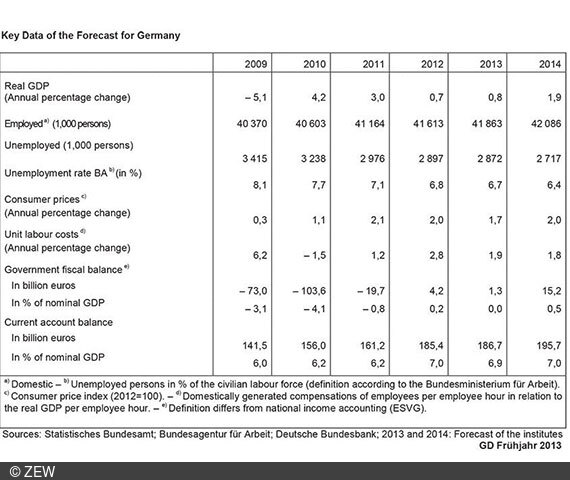

Positive signals for the German economy in the spring of 2013: the financial market situation has eased and the headwind from the global economy is abating. The Joint Economic Report of spring 2013, conducted by ZEW in cooperation with other leading economic research institutes, forecasts an increase of the German gross domestic product of 0.8 per cent in the current year (68 per cent projection interval: 0.1 to 1.5 per cent) and 1.9 per cent in 2014.

The German economy is moving upward again in the spring of 2013. The financial market situation has eased because insecurity about the future of the European monetary union could be reduced. The global headwind is also diminishing. The institutes expect the German gross domestic product to increase by 0.8 per cent this year (68 per cent projection interval: 0.1 to 1.5 per cent) and 1.9 per cent in the coming year. The number of unemployed persons is likely to keep declining and will, on an annual average, range at 2.9 million this year and 2.7 million people next year.

The inflation rate will fall to 1.7 per cent in the current year rise to 2.0 per cent in 2014 due to the greater utilization of production capacities. In 2013, Germany will have an almost balanced national budget, and due to the more favourable economic situation, it will record a surplus of 0.5 per cent in 2014 in GDP. Economic policy should now refocus more distinctly on long-term strategies. Although structural adjustment processes have meanwhile started in embattled countries, institutional problems of the euro area could not be solved yet. The German national budget is also exposed to considerable strain due to demographic developments in the long term.

In spring 2013, the global economy has slightly recovered. The expectations of companies and consumers have already been improving since autumn, and industrial production as well as global trade has increased again over the past months. The fact that the disintegration of the eurozone is less likely due to the ECB’s intervention contributes to this development. Apparently this picture has not changed fundamentally despite the banking and financial crisis in Cyprus.

Overall conditions at financial markets have improved significantly since last autumn. The tensions in the eurozone, which emerged in the aftermath of the renewed aggravation of the sovereign debt crisis in the second half of 2012, have eased considerably. Since mid-2012 stock prices in the advanced economies have been growing substantially, and in some countries they have reached highs not seen in years.

Yet some burdens remain. In many advanced economies, the private sector is still struggling to adapt its debt level to the long-term income expectations, which have dropped in the course of the global financial crisis. The adaptation does not yet seem to be finished and will probably continue to slow down economic growth, even if there is some evidence that, meanwhile, strains are easing in the USA.

Even four years after the Great Recession public finances have not recovered significantly in the advanced economies. Budget deficits can only be reduced on a slow pace due to the mostly weak, sometimes even strongly recessive economic development. Furthermore, there is growing evidence that in some countries cost-cutting policy will be loosened. The financial policy of the eurozone is likely to stay restrictive even though deviations from target figures due to cyclical downturns will be tolerated in 2013.

The advanced economies continue their expansive monetary policy. The central banks of the USA and Japan have announced that they will keep interest rates on a low level and carry on quantitative easing measures until the economy has recovered considerably.

The institutes expect the global economy to gather some pace this year and the next. The economy in the eurozone will also slightly recover. In 2013, the increase in global production will probably reach 2.5 per cent and in 2014 some three per cent. Nevertheless, significant downward risks persist. It is a central assumption that the crisis in the eurozone will not intensify again. However, energetic commitment to reform efforts and their successful subsequent implementation in embattled countries is not guaranteed. If the structural adjustment processes in the embattled states in the euro area slowed down noticeably or even failed, this would trigger a great loss of confidence and heavily strain the economy.

In spring 2013, the German economy has turned upward again. The economic sentiment has brightened up noticeably since last autumn. This may be due to the fact that the financial market situation has eased since insecurity about the future of the European monetary union abated. Furthermore, headwind from the global economy has diminished as there are signs of accelerating expansion outside the euro area. However, this change of sentiment has neither had impact on incoming orders nor on industrial production up to now. In this respect, the hard indicators do not suggest a strong recovery of production in the first quarter of this year. Besides, adverse weather conditions had some impact and slowed down activity in February and March.

The institutes expect the overall economy to gather pace in the course of this year. Insecurities due to the results of the elections in Italy and the banking crisis in Cyprus, however, show that the crisis might still intensify, even if not to the same extent as last year.

Conditions are in place for boosting the total economic output. Interest rates, for example, are very low and conditions for lending are favourable. In addition, German companies are highly competitive on the world market and have a strong presence in high-growth emerging countries in Asia. Moreover, the German labour market still proves to be robust. The recent cyclical downturn hardly left any traces. Income prospects thus remain stable, which may support private consumption expenditure. Throughout this year, a gradual acceleration of foreign demand is likely, so the companies’ sales expectations will brighten up and their reluctance to invest will subsequently decrease. Apart from special factors such as weather conditions, the pace of economic recovery will accelerate in 2013. However, the annual average gross domestic product will grow by only 0.8 per cent due to the statistical shortfall (68 per cent projection interval from 0.1 to 1.5 per cent). Imports will likely increase more rapidly than exports. As far as the figures go, the increase of the gross domestic product is based solely on domestic use. The overall high pace of expansion will probably help to improve the situation on the labour market further. Employment will be rising and the annual average number of unemployed persons will range at 2.9 million. Price increases have recently eased; especially mineral oil products have become cheaper. This constitutes another reason why the inflation rate will reach only 1.7 per cent, thereby remaining below the 2012 level. This year’s national budget is expected to be nearly balanced after a slight surplus in the past year.

In 2014, the economy will probably gain momentum slightly, and capacity utilisation will rise. The improving economic situation of trading partners results in rising export numbers, which give significant impulses. After all, however, it is the domestic economic development which will be responsible for the upswing and animate the investment drive. House building in particular may benefit from the low interest rates. Due to substantially growing income, private consumption expenditures will probably rise more strongly than this year. All in all, the gross domestic product of 2014 is expected to increase by 1.9 per cent. The number of unemployed persons will shrink significantly and reach an annual average of 2.7 million. The inflation rate will reach 2.0 per cent due to the increase of capacity utilisation. The situation of public finance will continue to improve. Owing to the favourable economic development, the government will record a budget surplus of 0.5 per cent in relation to the gross domestic product. This forecast explicitly involves an uncertainty regarding the coming Bundestag elections in September 2013.

For some time, framework conditions for the German economy have been so stimulating that the gross domestic product might even increase slightly more than has been delineated in this report. The improvement of the economic sentiment indicators, which started last autumn, confirms this assumption. One reason for caution, however, is the fact that the sentiment among companies slightly deteriorated in March, not only in Germany but also in important trading-partner nations. The data on incoming orders and industry production do not yet signal a breakthrough either. Apart from the uncertainty about the current basic trend of the economy, the institutes assume that downward risks prevail. Although embattled countries have started to go through structural adjustment processes, some governments encounter great difficulties in implementing reforms. Reducing reform efforts and loosening the consolidation policy may bring about new turbulence.

Faced with the global financial crisis as well as with the European debt and confidence crisis, economic policy managed to buy some time by introducing a number of monetary and fiscal policy measures. That way, it was possible to stabilise the economic prospects of the eurozone for the time being. In Germany, the situation of public finance and the labour market currently appears rather favourable. This, however, should by no means conceal that central problems responsible for the crisis have not yet been solved and that crucial steps still have to be taken. Economic policy should focus more explicitly on the long-term development of the economy.

In this context, the European Banking Union constitutes a key element. In the process of forming this institution, the focus should rather be on the creation of a stabilised banking system than on the distribution of burdens generated by the current crisis. It is essential to enforce the unity of decision and liability, which is central to market economies. This includes in particular the fact that in times of crisis, owners and creditors have to bear losses before taxpayers are being held liable to prevent worse from happening. In the case of Cyprus, the inclusion of creditors was the result of a rather chaotic process. This should be a good reason to introduce predictable and credible regulations for reacting on financial instability of banks and states within the euro area. Such regulations might also help to escape the vicious circle of banks’ problems and a lack of capacity concerning the public debt.

The Federal Government of Germany points to successes in budgetary consolidation. On a closer look, however, the performance seems rather mixed. For on the one hand, the current “over-achievement” of the debt brake on the federal level is partly based on factors without sustainable effect; important factors in this context were low interest rates and bracket creep. On the other hand, it is foreseeable that the ageing of the society will pose major challenges for the public finance sector.

In terms of budgetary consolidation, but also in other policy sectors, efficiency considerations are falling behind. The budgetary consolidation was driven forward without setting “qualitative” priorities. Extra revenues achieved through bracket creep are partly used to increase consumptive government expenditures and subventions. Furthermore, the introduction of a nation-wide minimum wage is being discussed. The debate on this topic should clearly mention the conflicts between the objective of an efficient allocation and distribution goals. The turnaround in energy policy has impact on the production potential, too. It leads to a change in relative prices and a depreciation of parts of the economic capital stock. Particularly the latter is often not being considered enough in the public debate.

Germany should also take precaution to prevent such erroneous developments appearing in a number of embattled countries. This requires a careful public budget management as well as an attentive observation of private credit developments and debt levels in the coming years, in which the single European monetary policy is expected to unfold significant expansive effects in Germany. Possible erroneous developments could be, among other measures, counteracted using macroprudential tools.

The Joint Economic Forecast Group consists of

Institut für Wirtschaftsforschung Halle

in cooperation with:

ifo Institut – Institute for Economic Research at the University of Munich

in cooperation with:

KOF Konjunkturforschungsstelle at ETH Zurich (Business Cycle Research)

Kiel Institute for the World Economy

for the medium-term forecast in co-operation with:

Centre for European Economic Research (ZEW) Mannheim

in cooperation with:

Institute for Advanced Studies, Vienna

For further information please contact

Dr. Marcus Kappler, Phone +49 621/1235-157, E-mail kappler@zew.de